Picking an investment account in Gscfinanceville feels like choosing a lock without the key. You stare at the options. You read the fine print.

Nothing clicks.

Why is this so hard?

Because no one tells you what actually matters (not) the jargon, not the sales pitch, but your goals, your timeline, your taxes.

I’ve opened accounts here. Closed them. Paid penalties.

Learned the hard way. This isn’t theory. It’s what worked (and what didn’t) when I asked myself: Which Investment Account to Open Gscfinanceville?

You don’t need ten accounts. You need one that fits you. Not your neighbor.

Not some influencer. You.

Some people want growth. Others need income now. A few are saving for a house next year.

All of them need different accounts.

This guide cuts through the noise. No fluff. No fake urgency.

Just clear comparisons (IRA) vs. brokerage vs. HSA. How each works here, in Gscfinanceville.

By the end, you’ll know which account to open next. Not someday. Not after more research. Next.

And yeah. You’ll feel confident about it. Because confidence comes from clarity.

Not complexity.

Why Are You Investing?

I start every conversation about money with one question: why do you want to invest? Not what you hope happens. Not what your cousin did.

Why you.

You might be saving for retirement. Or a house. Or your kid’s college.

Or just trying to keep up with inflation. All valid. None are dumb.

But here’s the thing (I’m) not sure what your timeline is. Are you looking at less than five years? Five to fifteen?

Fifteen-plus? That changes everything.

A short-term goal needs safety. Cash or bonds. Not stocks.

A 30-year retirement plan? You can handle more risk. More growth.

More time to recover.

Which Investment Account to Open Gscfinanceville depends entirely on your why and your when.

Check out Gscfinanceville if you’re stuck sorting that out.

I’ve seen people open Roth IRAs for vacations. (Bad idea.)

I’ve seen others use savings accounts for retirement. (Also bad.)

What’s your goal?

And how soon do you need that money?

Be honest.

I am.

IRAs and 401(k)s: Pick One and Start

I opened my first 401(k) the day I got my first real job. No hesitation. No spreadsheet.

Just clicked yes.

You get a 401(k) through your employer. They might match part of what you put in. That’s free money.

Not “maybe” free money. Actual free money. If your employer matches 3%, put in at least 3%.

Anything less is leaving cash on the table. (And yes, I’ve done it. Felt dumb.)

IRAs are accounts you open yourself. No employer needed. Two kinds matter: Traditional and Roth.

Roth IRA uses money you’ve already paid taxes on. So withdrawals later? Tax-free.

Traditional IRA lets you deduct contributions now. You pay taxes later. When you withdraw in retirement.

Every penny.

Who picks which? If you’re making more now than you expect in retirement. Go Traditional.

If you’re early career or expect higher income later (Roth) wins. I chose Roth at 24. Still think it was right.

Contribution limits change yearly. For 2024, it’s $7,000 for IRAs. 401(k)s let you put in $23,000. Don’t sweat the exact numbers.

Just start.

Which Investment Account to Open Gscfinanceville? Start with your 401(k). Especially if there’s a match.

Then add a Roth IRA. That’s the combo I’d choose again. No debate.

Brokerage Accounts: Your Money, No Rules

I open brokerage accounts when I want to invest without retirement handcuffs.

They’re not for retirement only. They’re for anything. A house down payment.

A car. Just building wealth.

These are taxable accounts. You pay taxes on profits when you sell high. Simple as that.

(No magic tax shield here.)

You decide how much to put in. You decide when to pull it out. Zero limits.

Zero penalties.

I buy stocks. Bonds. ETFs.

Mutual funds. Whatever fits my plan.

No gatekeepers. No age restrictions. No hoops.

Which Investment Account to Open Gscfinanceville? Ask yourself: Do I need access before 59½? Am I saving for something real and soon?

If yes. This is your account.

Need help picking one? Or deciding if it fits your goals? Find the right financial advisor gscfinanceville can cut through the noise.

I’ve used them twice. Once for a home fund. Once for a business side-hustle.

Brokerage accounts don’t care about your timeline. Neither should you.

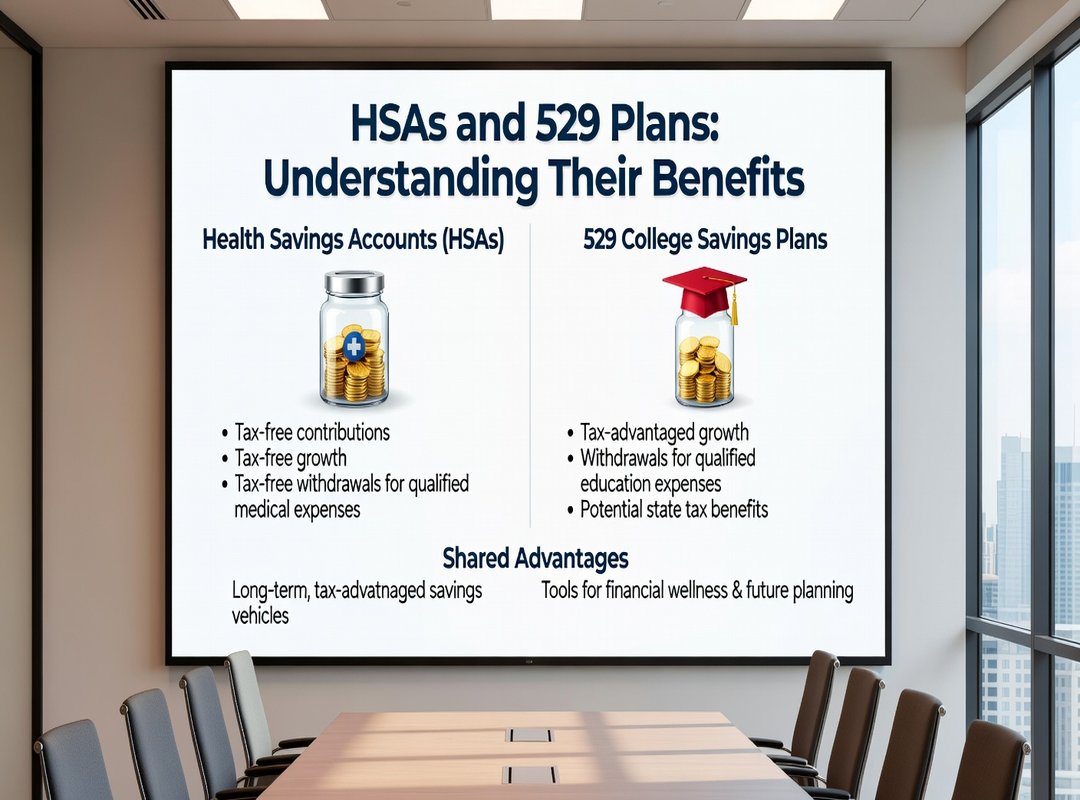

HSAs and 529s: Not Magic, Just Math

I opened an HSA the year my deductible jumped to $4,000.

It felt like getting punched. Then handed a tax break.

HSAs give you triple tax advantage. You deduct contributions. Growth is tax-free.

Withdrawals for real medical bills? Also tax-free. (Yes, even tampons and therapy count.)

But here’s the catch. You must have a high-deductible health plan. No HDHP?

No HSA. Period.

Some people treat HSAs like retirement accounts after 65. You can withdraw for anything then (but) non-medical withdrawals get taxed like income. So it’s not really a stealth IRA.

529 plans are simpler: save for school, grow tax-free, spend tax-free on tuition, books, even computers. K (12?) Up to $10,000 a year in some states. Trade school counts.

Coding bootcamp? Maybe (check) your state rules.

Which Investment Account to Open Gscfinanceville depends on your actual life. Not what sounds smart. Got a kid with college coming up? 529 makes sense.

Facing sky-high medical costs now? HSA moves first. You’re not failing if you skip both.

Not every account fits every person. And that’s fine.

Pick Your Account. Start Today.

I picked my first account blind. It was dumb. You don’t have to.

Ask yourself: What are you saving for? How soon do you need the money? How much tax paperwork will actually stress you out?

If you’ve never bought a stock or opened a Roth IRA (start) small. A $50 monthly deposit into a low-fee index fund counts. It builds habit before it builds wealth.

Gscfinanceville has real advisors. Some work downtown. Others serve you online.

You don’t need perfection. You need a place to begin.

The “best” account isn’t universal. It’s yours. Based on your life (not) some brochure.

Which Investment Account to Open Gscfinanceville?

That answer lives in your goals, not Google.

Need help finding someone local?

Check out Where Can I Find Financial Advice Gscfinanceville

Your Account Choice Starts Now

I opened my first IRA at 23. I messed it up twice before I got it right. You don’t need perfect knowledge to start.

You just need to pick one account that matches what you’re actually trying to do.

You now know the difference between retirement, general, and specialized accounts. That’s more than most people ever learn. Choosing wrong slows you down.

Choosing right puts your money to work today.

So ask yourself: What’s the goal? Buying a home in five years? Retiring at 60?

Saving for a kid’s college?

Which Investment Account to Open Gscfinanceville isn’t a puzzle to solve forever.

It’s a decision to make this week.

Don’t wait for “someday.”

Open an account that fits your goal (then) fund it.

You’ll feel lighter the second you hit submit.